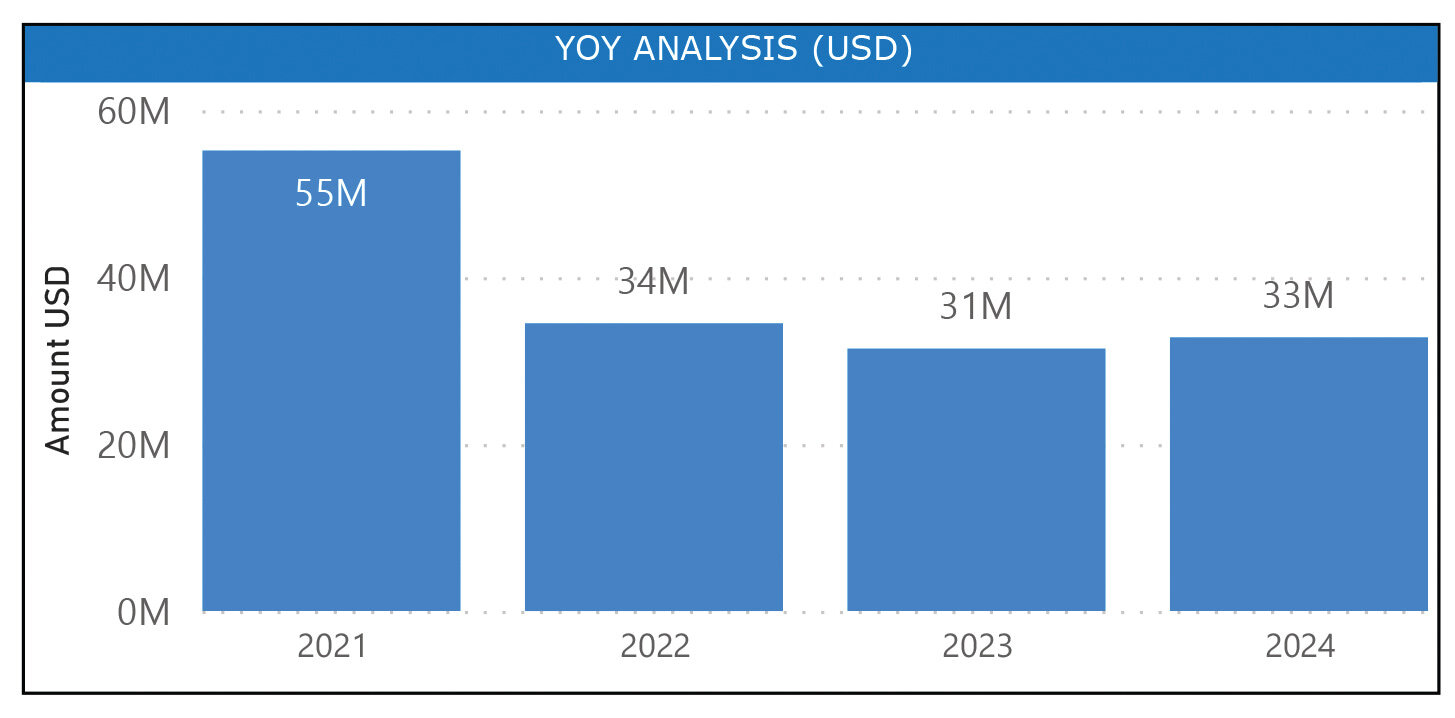

Slower than expected firearms sales during the first quarter of 2024 have many in the industry feeling uncertain about the rest of the year. Despite March marking the 56th straight month with gun sales topping 1 million and being in the top seven for that month since records have been kept, the fact is that this March’s gun sales fell back to pre-pandemic levels.

According to the National Association of Sporting Goods Wholesalers’ SCOPE program, Q1 2024 NICS checks were down 4% compared to 2023, and March was down 8% compared to the previous year.

For some background, the SCOPE program is designed to help industry members maximize profits by getting important, useful and, above all, accurate firearm industry sales information into their hands. The three programs—SCOPE PLX, SCOPE DLX and SCOPE CLX—are part of an industry-owned, distributor-led initiative to collect and analyze data that strengthens shooting sports businesses.

SCOPE data currently comes directly from 20 wholesalers of firearms, ammunition, optics and accessories. With about 65% of gun sales flowing through this channel, the SCOPE information represents the largest data sample anywhere in the industry.

To help shooting sports retailers maximize profits, we’ll be doing a number of reports on information available through SCOPE.

SO, WHAT’S UP?

To see what’s hot and what’s not we have to take a deeper dive into the data. Fortunately, the SCOPE program allows us to do that and share the data with Shooting Sports Retailer readers.

Overall, firearms sales in Q1 were down 8.79% from 2023. However, they were down 16.16% from the three-year average. At the retailer level, NICS checks were down 4.4% in Q1 compared to Q1 2023, and down 7.4% in March compared to the same month last year.

Concerning different firearm types, handgun shipments continued their year-over-year decline in Q1, finishing down about 10% from 2023. Some 83% of handguns shipped were semi-automatic, and, interestingly, 56% of handgun shipments were 9mm. Revolvers were again a bright spot in handguns, as they continue to grow somewhat.

Rifles, which are about 25% of firearm shipments, showed a continued but slowing growth and were up 7.5% compared to Q1 2023. About one-third of rifle shipments were bolt action, with 23% being lever action. About 19 percent were rimfire, including 17% that were chambered in .22 LR. While the bolt guns are still where the volume is, lever actions continue to gain in percentage. Lever action has become the number two rifle segment with 23% of shipments in Q1 2024. Increased inventory availability across the brands is giving the retailer a broad selection to build assortments.

SCOPE considers modern sporting rifles (MSRs) as a separate category, and MSR’s have continued to drop since they experienced a nice surge at the end of last year. Year-over-year, MSRs were down 11%, after falling in February. With the higher price points, consumers seem to be choosier about what models they want. Just over half of MSR shipments were chambered in .223/5.56, and 85% were AR-style rifles.

As for shotguns, shipments were pretty flat, falling 1% year-over-year. A strong aspect for shotguns, however, is that based on the rate of sale less than 10% or inventory remains. Considering all of the different categories — semi-autos, pump, doubles, etc. — that’s not a lot of inventory. Just over 40% of all shotgun shipments were semi-automatic, with 33% being pump action. As in the past, tactical shotguns have stayed strong. For pump guns, the ratio is 60:40 field guns, while for semi-autos it is 40:60 tactical scatterguns.

“High-end semi-automatic tactical guns are shipped as fast as inventory becomes available,” the report stated. “Retailers are right-sizing inventories and not buying back to the current rate of sale. Assortments are being built and open to buy dollars held for emerging trends.”

REGION BY REGION

Of course, shipments vary by region, and regional information can be interesting to analyze when making firearm stocking decisions.

In the West, shipments of all firearms were down 6% in Q1 compared to Q1 2023. Rifles leveled off at 24% share of product mix, and 48% of all shipments were semi-automatic handguns. Also in the West, handgun shipments were down 8.2%, rifles were up 3%, MSRs were down 11% and shotguns were down 9%.

For the Midwest region, shipments were down 5% compared to Q1 2023. Rifles maintained 29% of the mix, and semi-auto handguns were 40% of all firearm shipments. Handguns were down 10% year-over-year, rifles excluding MSRs was up 9%, MSRs were down 18% and shotguns were flat, unchanged from last year.

In the South, shipments of all firearms were down 4%, with rifles continuing to gain share of product mix. In that region, 47% of all firearm shipments were semi-auto handguns. Handgun shipments were down 9% year-over-year, rifles excluding MSRs were up 12%, MSRs were down 5% and shotgun shipments were flat.

In the Northeast region, shipments of all firearms were down 5%, with 45% of all firearms shipped being semi-automatic pistols and 35% of total firearms being 9mm. Again, shotguns were flat, rifles excluding MSRs were flat, MSRs were up 13% and shotgun shipments were flat.

AMMUNITION: A BRIGHT SPOT

While firearms overall are somewhat flat, ammunition represented a bright spot in Q1 2024, according to the report.

“Ammunition shipments increased 23% in Q1 2024 compared to 2023,” the report stated. “Inventory weeks of supply are low at approximately 10 weeks. The rolling 13-week average shipments continued to increase through Q1 2024. Overall shipments in the quarter stayed at increased levels.”

October kicked off a Q4 with some of the strongest shipments in the past three years. However, ammo shipments normalized to 2023 levels in March.

Centerfire pistol and rifle shipped at 50-50 levels, with top calibers, .223 Rem/5.56 NATO and 9mm making up the highest percentage of all calibers. Retail distribution shelves are recovering, but it will take time to restore inventory to all calibers/pack sizes on the retail shelf.

“The customers are buying based on need vs. panic,” the report said. “Pent-up demand from Q4 2023 mini surge did carry over to 2024.”

The report warned, however, that there may be some stressors on the ammo market in the upcoming short term.

“Powder availability may impact the consumer retail market,” the report stated. “Ukraine, the Israeli-Hamas conflict and other military needs are consuming large quantities of powder. Will there be supply issues or limited shipping from international suppliers?”

On a regional basis, ammo shipments in the West were up 12%. Centerfire ammo was up 14%, with a 50-50 pistol-to-rifle share. In the Midwest, overall ammo shipments were up 13%, with 57% centerfire rifle compared to 43% handgun. In the South, ammo shipments were up 15% compared to Q1 2023, with centerfire ammo being 57%. Some 23% was 9mm, and 22% was .223/5.56. In the Northeast, ammo shipments were up 15% overall. Centerfire ammo increased in share year over year, with 42% 9m and 38% .223/5.56.

AND WHAT ABOUT OPTICS?

Optics represented another fairly bright spot in Q1 2024. Overall, optics shipments were up 6% compared to 2023, although they were down 15% compared to the three-year average. Shipments were driven by observation optics, like binoculars, which were up 25%. For the quarter, riflescopes and reflex sights drove more than 60% of optics shipment dollars.

“Riflescopes' average weekly shipments fell steadily through Q1 2024,” the report stated. “Overall riflescope shipments have been declining since November 2023. Reflex sights are a bright spot in optics. Their inventory weeks of supply have been declining since October 2023.”

On a regional basis, in the West optics overall were down 17%, with observation optics flat, scopes down 33% and reflex sights down 50%. In the Midwest region, shipment of optics was up 11% overall, observation optics doubled from first quarter 2023, scopes were flat and so were reflex sights. In the South, overall optics shipments were up 15% over Q1 2023, with observation optics doubling, scopes flat and reflex sight shipments flat. In the Northeast, overall optics shipments were about the same as Q1 2023. Observation optics were up 33%, scopes were flat and reflex sights were about the same as in Q1 2023.

WRAPPING IT UP

All of that data raised a number of questions as Q2 2024 kicked off. Are people waiting for new products to launch, which typically begins in April? Will we begin seeing growth when those new products hit the shelves? Have manufacturers caught up with their production goals? And what about supply chain issues?

In the end, no matter what you sell in the firearms industry — guns, ammo, optics or all three — uncertainty is making retailers study the available data and make more discerning choices about what guns and related products they are purchasing as 2024 continues.

“Retailers are cautious and not buying back at the same rate they are selling through,” the report concluded. “Regulatory changes or potential changes, election concerns, the economic environment, world events and changes in historical demand are impacting the distribution and retail side of the equation.”